Market Decision Intelligence: Why Better Data Does Not Create Better Decisions

- Jun 1

- 39 min read

Updated: Jun 7

Executive Summary

For most of modern business history, market intelligence was built around a simple assumption: better information should lead to better decisions. When organizations lacked visibility into customers, competitors, demand, pricing, and market structure, this assumption made sense. Information was scarce, difficult to collect, expensive to analyze, and often unavailable to smaller companies. In that environment, the organization with better data often had a meaningful advantage.

That environment no longer exists.

Today, companies operate in a world of information abundance. Search behavior can be measured. Competitor activity can be tracked. Customer journeys can be analyzed. AI systems can summarize, classify, and interpret large quantities of market data in seconds. Executives, founders, investors, and agencies now have access to more information than at any previous point in business history. Yet despite this abundance, strategic decisions continue to fail at a familiar rate. Markets are entered too early or too late. Growth budgets are allocated toward channels that generate visibility but not value. Products are launched into categories that appear attractive in research but fail under real commercial pressure. Investors see demand signals, yet later discover that the market was active without being truly decision-ready.

This creates a central paradox: organizations have more data than ever, but not necessarily better decisions.

The reason is that information and decisions are not the same thing. Information describes what exists. Decisions determine what deserves commitment. Information expands options. Decisions narrow them. Information can reveal demand, traffic, competitors, and trends, but it does not automatically explain whether action is justified. Between data and commitment lies a difficult interpretive layer where assumptions, constraints, risk tolerance, responsibility, and judgment determine whether a market signal becomes a real decision.

Market Decision Intelligence is designed to operate in that layer.

It does not replace market research. It extends it. Traditional market research asks what is happening in a market. Market intelligence asks why it is happening. Market Decision Intelligence asks a more consequential question: does the available evidence justify responsible commitment?

This distinction matters because many markets create attention without commitment. Search demand may exist without willingness to pay. Traffic may increase without monetization. Competitors may appear fragmented while attention is already structurally controlled. A category may be highly visible while still failing to support accountable, budgeted, non-trivial decisions. In such cases, more data does not solve the problem. What is required is a stronger decision framework.

Market Decision Intelligence evaluates whether demand survives responsibility, whether uncertainty is bounded, whether monetization is structurally plausible, whether competitive pressure can be overcome, and whether execution is feasible under real-world constraints. Its purpose is not to predict the future with certainty. Its purpose is to clarify whether action is justified despite uncertainty.

As AI continues reducing the cost of information production, the value of human judgment increases. Reports will become easier to generate. Data will become easier to collect. Summaries will become cheaper. But deciding what matters, what deserves commitment, and what should be avoided will become more important, not less.

The future advantage will not belong only to organizations that know more. It will belong to organizations that decide better.

Introduction

The Paradox of Modern Markets

Modern organizations are surrounded by signals. A founder evaluating a new market can access keyword data, competitor research, market forecasts, customer reviews, pricing benchmarks, social media trends, AI-generated summaries, and website analytics before making a single strategic move. An executive allocating a growth budget can review traffic trends, conversion rates, content gaps, paid media benchmarks, and industry reports in a matter of hours. An investor assessing a category can analyze search demand, funding activity, public narratives, competitor positioning, and customer adoption signals with a level of visibility that would have been impossible a generation ago.

On the surface, this should produce better strategic decisions. More information should reduce uncertainty. More visibility should reduce risk. More analysis should improve judgment. Yet in practice, the opposite often happens. The volume of available information increases, but clarity does not increase at the same rate. Decision-makers become more informed, but not necessarily more certain. Dashboards become larger, reports become longer, and analysis becomes more sophisticated, while the fundamental question remains unresolved: what decision does this evidence actually justify?

This is one of the central problems in modern market intelligence. The issue is no longer that organizations cannot observe markets. The issue is that observation is often mistaken for understanding, and understanding is often mistaken for decision readiness. A company may know that search demand exists, but not whether that demand is monetizable. It may know that competitors are present, but not whether those competitors hold defensible attention. It may know that a trend is growing, but not whether the trend can support durable business value. It may know that users are interested, but not whether they are willing to commit.

The difference between these questions is not academic. It determines whether capital is allocated wisely or wasted. It determines whether a founder enters a market with structural potential or a market that merely looks attractive. It determines whether a growth initiative is built around decision-stage demand or around vanity visibility. It determines whether a strategy is supported by evidence or merely surrounded by data.

The traditional response to uncertainty is to collect more information. This response feels rational because it has worked in the past. When information was scarce, more data often did improve decisions. But in today’s digital environment, additional information frequently produces diminishing returns. After a certain point, the problem is not that the organization lacks data. The problem is that it lacks boundaries for interpreting data.

Without decision boundaries, information can create confidence without clarity. A large dataset can make a weak conclusion feel rigorous. A detailed report can make assumptions feel proven. A sophisticated forecast can make uncertainty appear smaller than it really is. This is where many strategic mistakes begin. The decision is not wrong because no analysis was performed. The decision is wrong because the analysis did not define what had to be true before action was justified.

Market Decision Intelligence begins from this gap. It assumes that the purpose of research is not merely to describe markets, but to support responsibility-bearing decisions under uncertainty. It treats data as a starting point, not as a conclusion. It recognizes that market signals do not carry meaning on their own. Meaning emerges only when signals are interpreted through decision questions: Is this demand real or merely visible? Is the market structurally monetizable? Are users exploring or committing? Can competition be overcome? Can the opportunity be executed within real constraints? What must be true before investment is justified?

These questions shift the role of market intelligence. The objective is no longer simply to know more. The objective is to decide better.

That shift is the foundation of Market Decision Intelligence.

The Decision Intelligence Flow

From Signals to Outcomes

Decision Intelligence Flow

Most modern analysis assumes that decisions emerge naturally from information. The implicit belief is that if enough data is collected, structured, and reviewed, a correct decision will eventually become obvious. In reality, decisions do not emerge from information automatically. They pass through a sequence of interpretation, evaluation, pressure, and commitment before they become visible as market outcomes.

Market Decision Intelligence views this sequence as a structured flow.

Data

↓

Information

↓

Interpretation

↓

Decision State

↓

Decision Boundaries

↓

Commitment

↓

Market Outcome

Each stage plays a different role.

Data is the raw signal layer. It includes search queries, keyword volumes, competitor visibility, traffic behavior, customer questions, pricing patterns, social discussion, conversion metrics, and market activity. Data is observable, but it is not yet meaningful. A rise in search volume may indicate demand, curiosity, fear, confusion, comparison, or temporary hype. On its own, data does not explain which of these interpretations is correct.

Information emerges when data is cleaned, organized, classified, and placed into a usable structure. Keywords may be grouped by intent. Competitors may be mapped by category. Demand may be segmented by funnel stage. Trends may be visualized over time. This improves visibility, but it still does not solve the decision problem. Information tells us what can be observed, not what should be done.

Interpretation is the point at which judgment begins. Signals are evaluated through context, business logic, economic reasoning, market structure, and human understanding. A keyword with high volume may be low value if it reflects informational curiosity rather than commercial intent. A competitor with high visibility may be less threatening if its traffic does not sit near the decision stage. A market with growing demand may still be unattractive if monetization remains weak. Interpretation turns structured information into strategic meaning.

Decision State describes where the market, customer, or category sits in its readiness cycle. Is the market dormant? Is it questioning legitimacy? Is it framing risks? Is it assigning accountability? Is it already acting? Different states require different conclusions. A market filled with curiosity is not the same as a market ready for commitment. A market discussing consequences is not the same as a market allocating budgets. Understanding the decision state prevents analysts from confusing early attention with mature demand.

Decision Boundaries are the conditions that must be satisfied before action becomes rational. They define the point at which uncertainty becomes acceptable relative to potential reward. A company may require evidence of monetization. An investor may require proof of repeatable commitment. An executive may require confidence that the opportunity can be executed without disproportionate complexity. If these boundaries are not crossed, the presence of demand alone is not enough.

Commitment occurs when responsibility is accepted. Resources are allocated. Budgets are approved. Contracts are signed. Products are adopted. Teams are assigned. Capital is deployed. Commitment is the point where interest becomes consequence. This is the layer most traditional analysis underestimates, because it is easier to measure attention than responsibility.

Market Outcome is the visible result: growth, adoption, revenue, churn, regulation, category expansion, market entry, or failure. Most market research focuses heavily on outcomes, but outcomes are late signals. By the time they are obvious, the underlying decision process has already taken place. Market Decision Intelligence therefore focuses not only on outcomes, but on the earlier stages that determine whether outcomes are likely to emerge.

This flow explains why two organizations can examine the same market and reach different decisions. They may possess similar data and similar information, but interpret the decision state differently. They may apply different boundaries. They may have different levels of risk tolerance. They may disagree about whether commitment is justified. The market itself has not changed. The decision logic has.

The purpose of Market Decision Intelligence is to make that logic explicit.

It does not claim that uncertainty can be eliminated. It does not claim that markets can be predicted with certainty. Instead, it provides a structured way to ask whether the journey from data to commitment is supported by enough evidence to justify action.

This is the difference between being data-informed and decision-ready.

The Evolution of Market Research

From Information Scarcity to Decision Scarcity

For much of the twentieth century, market research existed in a world of information scarcity. Companies did not have easy access to customer behavior. Competitor activity was difficult to observe. Market trends developed slowly and were often detected late. Consumer preferences had to be discovered through surveys, interviews, panels, focus groups, and field research. Data collection required time, money, and specialized expertise.

In that environment, the role of research was relatively clear: reduce ignorance. A company that understood its customers better than competitors had an advantage. A business that could estimate demand more accurately could make better expansion decisions. An organization that could identify customer preferences before launching a product could reduce risk. Research was valuable because visibility itself was valuable.

The early logic of market research was therefore built around access. The more information an organization could obtain, the better positioned it was to make decisions. This logic was reasonable because information was difficult to acquire. A well-executed research project could reveal insights that competitors did not have. In a world where many decisions were made with limited visibility, better information often improved strategic judgment.

The internet changed this environment completely. Digital behavior created new forms of market visibility. Search engines revealed what people were asking. Analytics platforms revealed how users moved through websites. Advertising platforms revealed which messages attracted attention. E-commerce platforms revealed purchase behavior. Social platforms revealed language, sentiment, and cultural shifts. Suddenly, markets became observable at a scale and speed that traditional research methods were never designed to handle.

This was a breakthrough, but it also created a new problem. When information became abundant, the challenge shifted from collection to interpretation. Organizations no longer struggled only to obtain signals. They struggled to understand which signals mattered. Search demand could be measured, but its economic meaning was uncertain. Traffic could be tracked, but its relationship to revenue was not always clear. Competitor visibility could be mapped, but visibility did not always equal competitive power. The availability of digital data expanded dramatically, but the ability to convert data into decision-quality judgment did not expand at the same pace.

Artificial intelligence has intensified this shift. AI tools can now summarize markets, cluster keywords, classify competitors, draft reports, identify patterns, and produce analysis at extraordinary speed. This reduces the cost of information production. It also reduces the uniqueness of information itself. When many organizations can access similar tools, generate similar summaries, and review similar data, competitive advantage can no longer come primarily from having information.

The advantage moves elsewhere.

It moves to judgment.

This is why modern organizations increasingly face decision scarcity rather than information scarcity. They do not lack signals. They lack confidence about what those signals justify. They do not lack research. They lack boundaries. They do not lack analysis. They lack a disciplined way to distinguish visibility from viability, interest from commitment, and demand from decision readiness.

This is the context in which Market Decision Intelligence becomes necessary. It is not a rejection of market research. It is a response to the limits of descriptive analysis in an environment where information is abundant and decisions remain difficult.

Traditional market research asks: What is happening?

Market intelligence asks: Why is it happening?

Market Decision Intelligence asks: Does this justify commitment? This reflects the broader shift in how market research is evolving from data collection into decision support.

That final question is becoming the central question of modern strategy.

The Economics of Decision-Making

Why Markets Are Ultimately Decision Systems

Most market analysis begins with markets.

Market size.

Market demand.

Market growth.

Market share.

Market trends.

Competitive structure.

Customer behavior.

These concepts are useful, but they describe the visible surface of market activity. They show what is happening after decisions have already begun to shape behavior. They tell us where attention is moving, where money is flowing, where competitors are positioned, and where customers appear to be active. But they often fail to explain the deeper mechanism beneath market outcomes.

Before there is a market outcome, there is a decision.

Before a customer purchases, someone decides that the product is worth the cost. Before a company enters a new geography, someone decides that the uncertainty is acceptable. Before an investor allocates capital, someone decides that the potential return justifies the risk. Before a product category grows, enough people decide that the category deserves time, trust, money, and behavioral change.

This means that markets are not only economic systems. They are decision systems.

Every market is made of thousands, sometimes millions, of decisions. Some are small and reversible: a user clicks, compares, reads, tests, or subscribes to a newsletter. Others are larger and more consequential: a team signs a contract, a founder enters a market, an investor funds a category, a board approves expansion, or a customer switches from an incumbent solution to a new one. The more consequential the decision, the more pressure it carries. Budget, accountability, uncertainty, reputation, switching cost, and responsibility all become part of the equation.

This is where many market analyses become too shallow. They measure activity without understanding the decision pressure behind that activity. A market may look active because people are searching, reading, comparing, and discussing. But if those behaviors do not convert into commitment, the activity may represent curiosity rather than readiness. From the outside, curiosity can look like demand. From the decision layer, it is something weaker.

The central question is therefore not only whether a market exists. It is whether the market allows decisions to happen.

A category may have demand but no commitment. It may have visibility but no trust. It may have traffic but no willingness to pay. It may have user interest but no budget owner. It may have strong public conversation but weak economic follow-through. In these cases, the market is not necessarily empty. It may even be noisy. But the decision system inside the market is not mature enough to support responsible action.

Market Decision Intelligence begins with this distinction. It treats market signals as evidence of decision behavior, not merely as indicators of interest. Search volume is not just a number. It may reflect curiosity, fear, comparison, urgency, dissatisfaction, or purchase intent. Competitor visibility is not just a ranking pattern. It may reflect authority, habit, trust, or structural control of attention. A trend is not only a trend. It may represent early questioning, broad normalization, or late-stage commitment.

The task is to understand what kind of decision environment those signals reveal.

This is why the economics of decision-making matter. Organizations do not act when uncertainty disappears. They act when uncertainty becomes acceptable. A market does not become attractive when all risk is removed. It becomes attractive when the possible reward justifies the remaining risk. Customers do not buy when they know everything. They buy when they know enough. Investors do not fund because the future is certain. They fund because the uncertainty appears bounded.

Decision quality therefore depends on how uncertainty is interpreted, not on whether uncertainty exists.

Traditional research often tries to reduce uncertainty by collecting more information. That can help, but only to a point. After enough information has been gathered, the remaining challenge is judgment. The decision-maker must still ask: Is this enough? Is the risk acceptable? Is the timing right? Is the upside real? Are the constraints manageable? What happens if we are wrong?

Those questions do not belong only to research. They belong to decision intelligence.

Bounded Rationality and the Limits of Optimization

A common mistake in business analysis is assuming that people make decisions as rational optimizers. In this view, customers compare every option, evaluate every feature, calculate every trade-off, and choose the objectively best solution. Investors examine all available evidence and allocate capital to the highest expected return. Executives weigh all strategic options and select the one with the strongest risk-adjusted outcome.

This is not how real decisions usually work.

Human beings operate with limited time, limited attention, limited information, limited memory, and limited tolerance for complexity. Organizations do the same. Even when a company has access to huge amounts of data, its decision-makers cannot process everything equally. They simplify. They prioritize. They ignore some signals and overemphasize others. They rely on frameworks, narratives, instincts, incentives, and past experience.

The concept of bounded rationality explains this reality. Decision-makers do not usually optimize. They satisfice. They look for an option that is good enough under the circumstances, not necessarily the perfect option in absolute terms. The decision is made when the available evidence crosses an acceptable threshold.

This has enormous implications for market intelligence.

If real decision-makers are not pure optimizers, then the role of intelligence is not simply to identify the “best” market, “best” keyword, “best” competitor gap, or “best” opportunity. The role of intelligence is to clarify when an option becomes sufficiently justified under real constraints.

A founder does not need perfect certainty before entering a market. But the founder does need enough evidence that demand is real, monetization is plausible, competition is manageable, and execution is possible. An executive does not need every risk eliminated before approving a growth initiative. But the executive does need confidence that the initiative is aligned with business value rather than vanity performance. An investor does not need a risk-free category. But the investor does need evidence that the market can support responsibility-bearing adoption, not just interest.

This is why the concept of “enough” is so important.

Most bad decisions are not made because no information existed. They are made because decision-makers believed they had enough evidence when they did not. A market looked attractive because demand was visible. A strategy looked reasonable because competitors were growing. A channel looked promising because traffic was available. A category looked investable because attention was increasing.

But attention is not enough. Visibility is not enough. Activity is not enough.

The real question is whether the evidence crosses the right decision boundaries.

Bounded rationality means that people will act before certainty is complete. That is unavoidable. Business requires decisions under uncertainty. Waiting for perfect information usually means waiting too long. But acting too early can be just as dangerous. The challenge is not to remove uncertainty completely. The challenge is to know whether the remaining uncertainty is acceptable.

This is precisely where Market Decision Intelligence adds value.

It does not promise perfect knowledge. It creates a more disciplined way to judge whether imperfect knowledge is sufficient for action.

The Cost of Being Wrong

Most market analysis focuses heavily on upside.

How large is the market?

How fast is it growing?

How much demand exists?

How much traffic can be captured?

How much revenue could be generated?

How much market share is available?

These are important questions, but they are incomplete. Decision-makers do not evaluate upside alone. They also evaluate the cost of being wrong.

This is especially true when decisions carry responsibility. A founder who enters the wrong market may lose months or years of effort. An executive who misallocates a growth budget may weaken internal trust and reduce future strategic flexibility. An investor who funds a category too early may lock capital into a market that is active but not investable. An agency that recommends a direction based on surface demand may damage credibility if the market fails to convert.

The cost of being wrong changes the decision.

A low-risk experiment can be justified with limited evidence. A high-stakes market entry cannot - This is why not all decisions require the same depth of market intelligence. A small content test may only require directional signals. A major expansion decision requires deeper validation. A reversible decision can tolerate more uncertainty. An irreversible or capital-intensive decision requires stricter boundaries.

This is why the same market can produce different decisions for different actors.

A small founder may enter a niche because the downside is manageable and learning is valuable. A large company may avoid the same niche because the opportunity is too small relative to organizational complexity. A venture investor may reject a market because it cannot support scalable returns, while an operator may build a profitable business in the same category. The market did not change. The cost of being wrong changed.

Market Decision Intelligence must therefore consider who bears responsibility.

A market is not universally attractive or unattractive. It is attractive relative to a decision, a decision-maker, and a risk profile. This is why generic opportunity scores can be misleading. A keyword tool may identify “opportunity” based on volume, difficulty, and competitive gaps. But the business meaning of that opportunity depends on revenue proximity, intent, monetization, execution capability, and strategic fit.

An opportunity that is attractive for traffic may be irrelevant for revenue. An opportunity that is useful for brand awareness may not support investor-level commitment. An opportunity that appears strong in SEO terms may be weak in decision terms.

This is where many analyses fail. They treat opportunity as a universal property of the market. In reality, opportunity is decision-specific.

The same signal can mean different things depending on the decision being made.

A high-volume keyword may be valuable for a publisher but useless for a company seeking qualified buyers. A fragmented competitive landscape may indicate opportunity, but it may also indicate weak monetization and low barriers to entry. A fast-growing category may suggest momentum, but it may also signal hype, instability, and unclear willingness to pay.

The cost of being wrong forces analysis to move beyond surface optimism.

It asks: What happens if this interpretation is incorrect? What resources are exposed? How reversible is the decision? How long will it take to know? What assumptions must hold? What failure mode is most likely?

These questions are not pessimistic. They are responsible.

Strong market intelligence should not only identify upside. It should clarify downside, constraints, and exposure. It should help decision-makers understand not only what could work, but what must be true for it to work.

That is the difference between encouraging action and supporting judgment.

Why Forecasts Often Create False Certainty

Forecasts are among the most persuasive tools in business. They convert uncertainty into numbers. They give decision-makers something concrete to discuss. They create the appearance of structure. A forecast can show revenue growth over three months, six months, or twelve months. It can model conservative, realistic, and aggressive scenarios. It can make a strategy feel more disciplined.

But forecasts are often misunderstood.

A forecast is not the future. It is a structured expression of assumptions.

Every forecast depends on conditions. Demand must behave in a certain way. Competition must remain within a certain range. Execution must happen at a certain quality. Conversion rates must improve. Costs must stay manageable. Customers must respond. The market must not shift too dramatically. If those assumptions fail, the forecast fails.

The problem is not forecasting itself. Scenario-based forecasting can be highly useful when handled carefully. The problem is when forecasts are presented as outcomes rather than decision lenses.

A good forecast should not say, “This will happen.”

It should say, “This could happen if these conditions are true.”

That distinction changes everything.

Market Decision Intelligence treats scenarios as boundary tools. A conservative scenario clarifies what happens if execution is limited or demand capture is weak. A realistic scenario clarifies what happens if core assumptions hold. An aggressive scenario clarifies what happens if multiple favorable conditions align. The point is not to predict a single future. The point is to understand the sensitivity of the decision.

If a strategy only works in an aggressive scenario, it is fragile. If it produces value even under conservative assumptions, it is more resilient. If small execution gaps destroy the economics, the opportunity may be less attractive than it appears. If modest improvements create meaningful upside, the opportunity may be structurally strong.

Forecasts become useful when they reveal decision risk.

They become dangerous when they hide it.

This is why Market Decision Intelligence avoids treating projections as guarantees. The value of a scenario is not that it predicts the future. The value is that it exposes what must be true for the decision to make sense.

In other words, forecasting should not replace judgment.

It should discipline judgment.

Why Demand Is Not Enough

The Most Common Mistake in Market Analysis

If there is one mistake that repeatedly causes strategic failure, it is the assumption that demand equals opportunity.

The logic is simple and appealing. If people are searching for something, there must be demand. If there is demand, there must be opportunity. If there is opportunity, investment should be justified.

This logic is incomplete.

Demand is necessary, but demand is not sufficient.

A market can contain demand and still fail to support a strong business. A category can attract attention and still lack monetization. A product can generate curiosity and still fail to become a priority. A service can be searched frequently and still struggle to convert. A technology can receive enormous public interest and still remain outside budgeted, accountable adoption.

The reason is that demand exists at different levels of seriousness.

Some demand is informational. People want to understand a topic. Some demand is comparative. People want to evaluate options. Some demand is commercial. People are considering purchase. Some demand is transactional. People are ready to act. Some demand is strategic. Organizations are prepared to allocate budget, accept risk, and change behavior.

These forms of demand are not equal.

A thousand users searching “what is X” do not carry the same economic meaning as a hundred users searching “best X provider for enterprise teams.” A broad trend may generate awareness, but decision-stage demand determines whether money moves. High-volume curiosity can support media, education, and awareness, but it may not support a commercial model. Low-volume, high-intent demand can be far more valuable than massive top-of-funnel attention.

This is why demand must be interpreted, not merely measured.

Search volume tells us that people are asking. It does not tell us whether they are deciding. Traffic tells us that people are arriving. It does not tell us whether they trust, commit, or pay. Competitive activity tells us that companies are participating. It does not tell us whether the market produces durable value.

Demand becomes meaningful only when it is connected to decision behavior.

Interest Is Not Commitment

Interest is easy to create and easy to observe. Commitment is harder to create and harder to measure.

People express interest constantly. They read articles, watch videos, compare tools, attend webinars, download guides, sign up for trials, and ask questions. In digital markets, these behaviors create measurable signals. They look like engagement. They often appear positive in dashboards. They can make a market feel alive.

But interest does not carry the same weight as commitment.

Commitment means that something is at stake. A customer pays. A company allocates budget. A team changes its workflow. A buyer accepts switching costs. An investor deploys capital. An executive becomes accountable for the outcome. Commitment transforms curiosity into consequence.

This distinction explains why some markets appear strong from the outside but disappoint after investment.

A SaaS category may generate large numbers of free trials but weak paid conversion. An AI tool may attract heavy experimentation but limited workflow adoption. A consumer product may generate social attention but low repeat purchase. A consulting offer may receive many inquiries but few qualified buyers. In each case, interest exists. Commitment does not.

Market Decision Intelligence focuses on the gap between the two.

The critical question is not only, “Are people interested?”

The critical question is, “What level of consequence are they willing to accept?”

A user who reads a guide accepts almost no consequence. A user who books a consultation accepts more. A buyer who signs a contract accepts more. An organization that changes internal processes accepts much more. An investor who funds a category accepts a different level of consequence entirely.

The deeper the consequence, the stronger the decision signal.

This is why market analysis must classify signals by commitment level. Treating all engagement as equal leads to false confidence. A market with many low-commitment signals may be less attractive than a smaller market with fewer but stronger commitment signals.

Attention can make a market visible.

Commitment makes it real.

Visibility Is Not Viability

Digital markets reward visibility. Ranking on search engines, appearing in industry conversations, showing up in comparison lists, and generating traffic all create the impression of market presence. For many companies, visibility becomes a goal in itself. More impressions, more clicks, more visits, more mentions, more rankings.

Visibility matters. But visibility is not the same as viability.

A visible market is one that people can see. A viable market is one that can support economic activity under real constraints.

The difference is significant.

A company may rank for many keywords but fail to generate qualified demand. A site may attract traffic but lack revenue proximity. A category may appear popular but have weak pricing power. A competitor may dominate search results but depend on low-margin, low-retention customers. A trend may appear everywhere but lack durable willingness to pay.

Visibility answers the question: Can the market be observed?

Viability answers the question: Can the market support responsible action?

These are different questions.

The visibility trap occurs when organizations treat the first answer as if it proves the second. They see search demand and assume business potential. They see traffic and assume growth. They see competitor content and assume commercial value. They see category discussion and assume market maturity.

But many visible markets are economically weak.

Some are dominated by information-seeking behavior. Some are too price-sensitive. Some have unclear buyers. Some lack urgency. Some attract users who want free tools but will not pay. Some are structurally fragmented because no player can build enough trust or margin to dominate.

Market Decision Intelligence therefore treats visibility as an input, not a conclusion.

Visibility earns attention.

It does not automatically earn investment.

Demand Without Monetization Is Incomplete

One of the clearest boundaries in market analysis is the monetization boundary.

A market may show demand, but if that demand cannot be translated into economic value, the opportunity remains incomplete. This is common in digital categories. Users may want information, tools, convenience, entertainment, or access, but their willingness to pay may be weak. They may expect free options. They may switch frequently. They may resist subscriptions. They may compare heavily but delay purchase. They may value the solution, but not enough to support healthy margins.

In these cases, demand is real but economically insufficient.

This is especially important for investors and executives because monetization determines whether demand can support durable value. A market with huge attention but weak monetization may be less attractive than a smaller market with strong willingness to pay. A category with modest search volume but high contract value may be more valuable than a category with large traffic and low conversion. The economic meaning of demand depends on what happens after attention is captured.

Monetization requires several conditions. The buyer must recognize value. The problem must be important enough to justify payment. The solution must be trusted. The pricing must fit the perceived value. The decision-maker must have budget or authority. The purchase must be easier than the cost of inaction. The market must support margins after acquisition, delivery, and retention costs.

If these conditions are weak, demand remains fragile.

This is why content, keywords, and traffic should not be evaluated only by volume. They should be evaluated by revenue proximity. A low-volume keyword with strong purchase intent may be more valuable than a high-volume keyword with educational intent. A decision-stage article may create more business value than a broad awareness article. A comparison page may matter more than a general definition page if buyers are already close to action.

Market Decision Intelligence asks not simply whether demand exists, but whether demand can move through the economic system.

Can it become qualified interest?

Can it become trust?

Can it become purchase?

Can it become retention?

Can it become strategic value?

If the answer is no, demand alone is not enough.

Demand Without Responsibility Is Fragile

Even monetization is not the full story. In higher-stakes markets, the key issue is not only whether someone will pay. It is whether someone is willing to become responsible for the decision.

Responsibility is a stronger signal than payment alone.

A low-cost purchase may involve little responsibility. A monthly subscription may involve moderate commitment. A strategic software implementation involves more. A market entry decision involves much more. An acquisition, investment, or enterprise transformation carries significant responsibility.

The more responsibility a decision carries, the more demanding the market becomes. Buyers need trust. Executives need justification. Investors need confidence. Teams need alignment. Risk must be explained. Failure must be tolerable. Alternatives must be considered. The decision must survive internal scrutiny.

This is why high-stakes markets often move slowly despite clear demand.

The demand may exist, but the responsibility threshold is high.

For example, a company may know it needs better market intelligence. It may read articles, compare providers, download reports, and discuss the issue internally. But commissioning a strategic report, reallocating growth budget, or entering a new market requires accountability. Someone must justify the expense. Someone must defend the decision. Someone must act on the findings. Someone must own the outcome.

That is a different level of demand.

Market Decision Intelligence pays close attention to responsibility because it reveals the maturity of the decision environment. A market that produces many low-responsibility actions may be active but shallow. A market that produces fewer, higher-responsibility actions may be more valuable.

This distinction is central to understanding decision readiness.

A market becomes strategically meaningful when demand survives responsibility.

The Demand Ladder

One way to understand this is to think of demand as a ladder.

At the bottom is awareness. People know the category exists.

Above that is curiosity. People begin asking questions.

Above that is comparison. People evaluate alternatives.

Above that is intent. People begin considering action.

Above that is commitment. People accept cost, risk, and responsibility.

Above that is adoption. The decision becomes part of behavior, budget, or operations.

Many markets never reach the upper levels of the ladder.

They remain in awareness, curiosity, or comparison. This can still create traffic, content engagement, and public conversation. But it does not necessarily create economic value. A market only becomes commercially strong when enough people climb toward intent, commitment, and adoption.

This is why the strongest market signals are not always the largest. They are the signals closest to commitment. The practical way to test this is through the Decision Boundary Framework.

Searches that include pricing, providers, comparisons, alternatives, implementation, ROI, risks, or “best for” language often reveal more decision pressure than broad educational searches. Inquiries from budget owners matter more than casual readers. Repeat purchase matters more than first-click interest. Contract renewal matters more than trial signup. Strategic allocation matters more than public excitement.

The demand ladder helps explain why some content strategies fail. They attract readers but not decision-makers. They generate impressions but not qualified movement. They build awareness but not confidence. They answer questions that users ask early, but fail to support the questions buyers ask before acting.

For YNLIZE, this distinction is especially important. The goal is not to maximize traffic in isolation. The goal is to help founders, executives, agencies, and investors understand whether a market, strategy, or investment is worth pursuing under real constraints.

That requires decision-stage demand.

Not just demand.

Why Demand Analysis Must Become Decision Analysis

Demand analysis is still essential. No serious market evaluation can ignore it. But demand analysis must evolve. It should not stop at measuring whether people are searching, visiting, comparing, or discussing. It must ask what those behaviors reveal about decision readiness.

Are users learning or choosing?

Are they exploring or committing?

Are they comparing casually or evaluating seriously?

Are they seeking information or reducing risk before action?

Are they acting as individuals, buyers, executives, or budget owners?

Are they close to responsibility?

These questions transform demand analysis into decision analysis.

They force the analyst to interpret market behavior through the lens of commitment. They prevent teams from overvaluing surface activity. They help decision-makers distinguish between markets that are merely visible and markets that are structurally ready for investment, growth, or entry.

This is the reason Market Decision Intelligence places demand within a broader framework. Demand is the beginning of analysis, not the end. It must be tested against monetization, commitment, competition, and execution. Only then can it support a responsible decision.

The central principle is simple:

Demand creates attention. Decisions create markets.

Market Research vs Market Intelligence vs Market Decision Intelligence

Market Decision Intelligence is easiest to understand when it is separated from two related but different disciplines: market research and market intelligence.

The three are connected, but they do not answer the same question.

Market research is primarily concerned with visibility. It helps organizations understand what exists in a market: customers, competitors, categories, demand patterns, price points, behaviors, preferences, and trends. It is descriptive by nature. A good market research process reduces ignorance and gives decision-makers a clearer picture of the environment they are operating in.

Market intelligence goes one level deeper. It does not only ask what exists. It asks why market conditions are developing in a certain way. It interprets competitor behavior, demand shifts, positioning gaps, industry dynamics, growth patterns, and commercial pressure. Market intelligence is less about collecting facts and more about interpreting market structure.

Market Decision Intelligence introduces a third layer. It asks whether the evidence available is strong enough to justify commitment. Its primary concern is not description or interpretation alone. Its primary concern is decision quality.

This distinction matters because organizations often confuse these layers. They commission market research when they actually need decision support. They analyze competitors when they actually need to evaluate whether the market is worth entering. They measure demand when they actually need to understand whether that demand can survive budget ownership, risk, and responsibility.

A company may understand a market and still make a poor decision within it. An investor may understand a category and still misjudge its investability. A founder may identify demand and still enter too early. An executive may see growth potential and still allocate resources toward the wrong constraint.

Understanding is necessary.

It is not the same as decision readiness.

The Three Layers of Market Understanding

The difference between these disciplines can be summarized as follows:

Dimension | Market Research | Market Intelligence | Market Decision Intelligence |

Primary Question | What is happening? | Why is it happening? | Does this justify commitment? |

Core Function | Description | Interpretation | Decision justification |

Main Output | Findings | Insights | Decision boundaries |

Focus | Market visibility | Market structure | Decision readiness |

Typical Signals | Surveys, trends, customer data, keyword demand | Competitors, positioning, category dynamics, strategic shifts | Risk, commitment, monetization, feasibility, responsibility |

Success Measure | Better understanding | Better strategic context | Reduced decision risk |

Main Risk | Data without meaning | Insight without action | Acting before boundaries are crossed |

Best Used For | Learning the market | Understanding dynamics | Supporting high-stakes decisions |

This table is important because it prevents a common category mistake.

Many organizations believe they are doing decision intelligence when they are only doing research. They collect data, identify trends, summarize competitors, and produce conclusions. But unless the analysis defines what must be true before action is justified, it remains informational rather than decisional.

Market research might show that a category is growing.

Market intelligence might explain that growth is being driven by changing customer expectations, competitor fragmentation, or pricing pressure.

Market Decision Intelligence asks whether that growth justifies action for a specific decision-maker under real constraints.

That last step is where strategic value is often created or lost.

Why Market Research Alone Is Not Enough

Market research is valuable. No serious organization should make decisions without understanding the environment in which it operates. The problem begins when research is treated as if it automatically produces decisions.

A market research report may show that demand exists. It may identify customer segments. It may map competitors. It may estimate market size. It may describe customer preferences. These outputs are useful, but they are not the same as a decision recommendation.

For example, a market may be large but unattractive. It may contain many customers but low willingness to pay. It may grow quickly but remain structurally unprofitable. It may have fragmented competition because no player can build defensible advantage. It may show strong search volume because people are confused, not because they are ready to buy.

Market research often tells organizations where to look.

It does not always tell them whether to move.

That distinction becomes especially important in high-stakes decisions. A founder considering market entry does not only need to know whether demand exists. The founder needs to know whether demand can become revenue within the company’s constraints. An executive deciding whether to increase growth investment does not only need to know where traffic exists. The executive needs to know whether additional traffic will create economic value. An investor evaluating a category does not only need to know whether the category is visible. The investor needs to know whether the category can support responsibility-bearing adoption at scale.

Market research becomes insufficient when the decision carries consequences beyond learning.

The more irreversible the decision, the more important the decision layer becomes.

Why Market Intelligence Still Needs a Decision Layer

Market intelligence improves on market research by interpreting structure. It asks why demand is moving, why competitors behave as they do, why certain categories grow, and why some companies capture more value than others.

This is a meaningful upgrade.

But market intelligence can still stop too early.

A strong market intelligence process may produce excellent strategic insight while leaving the decision-maker with unresolved uncertainty. It may explain that a market is growing because customers are dissatisfied with incumbents. It may show that competitors are weak in decision-stage content. It may reveal that demand is shifting toward higher-value use cases. But the final decision still requires an additional layer of judgment.

Is the timing right?

Is the opportunity strong enough?

Is the risk acceptable?

Is the organization capable of execution?

Is the market structurally ready for commitment?

This is where Market Decision Intelligence enters.

It does not merely interpret the market. It tests whether the market supports the decision being considered.

The difference is subtle but powerful.

Market intelligence might say:

“This market is becoming more attractive.”

Market Decision Intelligence asks:

“At what point does this attractiveness justify commitment?”

Market intelligence might say:

“Competitors are under-serving this segment.”

Market Decision Intelligence asks:

“Can this segment be reached, converted, and monetized under real constraints?”

Market intelligence might say:

“Demand is increasing.”

Market Decision Intelligence asks:

“Is the demand moving toward responsibility-bearing action, or is it still exploratory?”

This is the layer most organizations need but rarely formalize.

Market Decision Intelligence Is Decision-Specific

One of the most important principles of Market Decision Intelligence is that opportunity is not universal.

The same market can be attractive for one decision-maker and unattractive for another.

A niche market may be ideal for a founder but too small for a venture investor. A traffic-heavy category may be useful for a publisher but weak for a product company. A fragmented competitive landscape may be attractive for an agile operator but irrelevant for a large enterprise with high overhead. A market with uncertain monetization may be acceptable for experimentation but unsuitable for capital-intensive expansion.

This means that the question “Is this a good market?” is often too broad.

A better question is:

Good for which decision, under which constraints, for which decision-maker?

Market Decision Intelligence is built around this level of specificity. It does not evaluate opportunity in the abstract. It evaluates decision readiness relative to a defined objective, risk profile, and execution context.

For a founder, the relevant decision may be whether to enter a market.

For an executive, it may be whether to allocate growth capital.

For an agency, it may be whether a client’s market has enough structural potential to justify a strategic program.

For an investor, it may be whether a category supports scalable, responsibility-bearing adoption.

Each of these decisions requires different evidence.

This is why generic opportunity scores are often misleading. They compress complexity into a number. They make different types of value appear comparable. They may consider volume, difficulty, and competition, but ignore commitment, monetization, execution risk, budget ownership, or strategic consequence.

Market Decision Intelligence resists this simplification.

It asks what decision is being made, who bears responsibility, what the cost of being wrong is, and which boundaries must be crossed before action becomes justified.

The Core Difference: Findings, Insights, and Boundaries

The easiest way to understand the distinction is to compare the outputs.

Market research produces findings.

A finding might be:

“This keyword cluster has strong search volume.”“Customers are comparing several providers.”“Competitors are publishing educational content.”“The category is growing.”

Market intelligence produces insights.

An insight might be:

“Search demand is growing because customers are dissatisfied with existing options.”

“Competitors dominate awareness-stage content but are weak at the decision stage.”

“The category is shifting from curiosity toward commercial evaluation.”

“Market fragmentation reflects weak authority rather than open opportunity.”

Market Decision Intelligence produces boundaries.

A boundary might be:

“Demand exists, but monetization is not yet proven.”

“Interest is active, but commitment remains weak.”

“Competitive pressure is manageable only if the company can differentiate around trust.”

“Execution risk is too high unless the offering is narrowed.”

“The market supports exploration but not full-scale investment yet.”

Boundaries are more useful than findings when a decision must be made.

They clarify what is known, what remains uncertain, and what must be true before action is justified.

This is the practical value of Market Decision Intelligence. It does not simply add more information to the decision-maker’s desk. It reduces ambiguity around commitment.

Decision States

How Markets Become Ready to Act

Markets do not usually change suddenly.

They appear to change suddenly because most organizations notice them late.

A product category seems to explode overnight. A technology appears to move from niche to mainstream. A regulatory issue suddenly becomes urgent. A consumer behavior rapidly normalizes. A competitor seems to become dominant very quickly.

But beneath the visible outcome, a slower process usually took place.

People began asking questions.

Those questions changed in tone.

Curiosity became evaluation.

Evaluation became concern.

Concern became accountability.

Accountability became action.

Action became normal.

This sequence matters because market outcomes are late signals. By the time revenue, regulation, adoption, or competitive movement becomes obvious, the underlying decision environment has already shifted.

Market Decision Intelligence therefore pays attention not only to outcomes, but to the language and behavior that precede outcomes.

The central assumption is simple:

Markets move through decision states before they produce visible market outcomes.

A decision state is the current stage of collective readiness around a market, category, product, risk, or opportunity. It describes whether the market is ignoring, questioning, evaluating, assigning responsibility, acting, or normalizing.

This is not sentiment analysis. It is not polling. It is not prediction in a narrow statistical sense.

It is a way of understanding where a market sits in its movement from awareness to action.

Why Decision States Matter

A market in early curiosity should not be interpreted the same way as a market near commitment.

Both may generate search activity. Both may produce content engagement. Both may appear in research tools. But they are not equivalent.

A person searching “what is market intelligence” is not in the same decision state as a founder searching “market entry research before launching in Germany.” A company reading about AI strategy is not in the same state as a team comparing enterprise AI implementation vendors. A consumer browsing “best coffee beans” is not in the same state as someone searching “coffee subscription delivery monthly.”

The surface behavior may look similar.

The decision pressure is different.

Decision States help interpret this difference. They classify the meaning behind market language. Instead of treating all demand as equal, they ask what stage of readiness the demand represents.

This is critical because the same keyword volume can mean very different things depending on the dominant question type.

Definition-based language suggests early understanding.

Risk-based language suggests concern.

Comparison language suggests evaluation.

Pricing language suggests monetization pressure.

Implementation language suggests operational seriousness.

Regulatory language suggests accountability.

“Best provider” language suggests proximity to choice.

A market’s language reveals its decision state.

When the dominant language changes, the market may be moving.

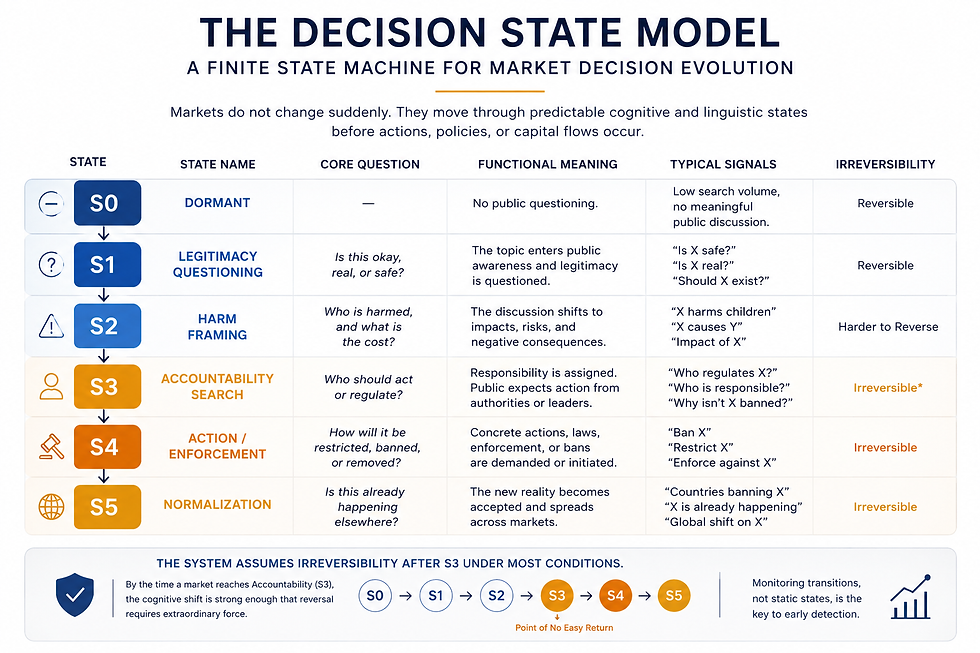

The YNLIZE Decision State Model

The Decision State Model maps market readiness across six stages.

S0 — DormantS1 — Legitimacy QuestioningS2 — Harm / Cost FramingS3 — Accountability SearchS4 — Action / EnforcementS5 — NormalizationThe model is not designed to predict exact outcomes. It is designed to diagnose where decision pressure is building and how far the market has moved from passive awareness toward action.

Each state represents a different level of readiness.

S0 Dormant

No Meaningful Public Questioning

In the dormant state, the market or topic exists but has not entered meaningful public questioning. There may be isolated signals, specialist discussion, or early technical awareness, but there is no broad decision pressure.

At this stage, the market is not yet asking serious questions.

There is little urgency.

There is little accountability.

There is little commercial pressure.

There is little evidence of commitment.

A dormant market may still contain future potential, but from a decision standpoint it remains undeveloped. Acting in this state usually requires a high tolerance for uncertainty. Investors may classify it as speculative. Founders may view it as early exploration. Executives may avoid major commitment because the market has not yet proven that enough people care.

The danger in S0 is overinterpretation. Early signals can be exciting because they appear undiscovered. But many dormant topics never transition into meaningful demand. The absence of competition may indicate opportunity, but it may also indicate that the market has not formed.

In S0, the correct decision is often not commitment.

It is observation, learning, and boundary definition.

S1 Legitimacy Questioning

“Is This Real, Useful, Safe, or Necessary?”

In S1, the market begins asking whether the topic deserves attention.

The language changes from silence to questioning.

People ask:

What is this?

Is it real?

Does it matter?

Is it safe?

Is it useful?

Is it legitimate?

Why are people talking about it?

This is the stage where many new technologies, services, and categories first become visible in search data. Curiosity rises. Educational content performs well. Definitions become important. Explanatory articles gain traction. Analysts and early adopters begin discussing the category.

But S1 is still not commitment.

It is legitimacy testing.

The market is trying to decide whether the topic deserves a place in its mental model. This can create misleading signals. Search volume may increase rapidly, but the demand may remain shallow. Users may consume content without being ready to act. Companies may discuss the category without allocating budget. Investors may track the space without deploying capital.

The danger in S1 is mistaking curiosity for demand.

A market can generate significant informational activity at this stage while remaining commercially immature. Many AI tools, emerging technologies, wellness trends, and B2B software categories pass through this stage with intense attention but uncertain monetization.

In S1, the key question is:

Is the market merely trying to understand the category, or is it beginning to evaluate consequences?

That transition leads to S2.

S2 Harm / Cost Framing

“What Is the Risk, Cost, or Consequence?”

In S2, the conversation becomes more serious.

The market is no longer asking only whether the topic is real. It begins asking what the topic means.

What are the risks?

Who benefits?

Who loses?

What are the costs?

What happens if this fails?

What happens if we ignore it?

What are the unintended consequences?

This stage is important because it indicates that the topic has moved beyond curiosity. The market is beginning to evaluate impact.

In commercial markets, this may appear as questions about ROI, pricing, implementation risk, switching cost, alternatives, limitations, or failure cases. In regulatory or social markets, it may appear as concern about harm, fairness, safety, compliance, or accountability. In investment contexts, it may appear as questions about durability, margins, retention, and category risk.

S2 can be positive or negative. The presence of risk language does not always mean rejection. In many cases, it means the market is taking the category seriously. People do not evaluate risk deeply for things they do not consider important.

The danger in S2 is assuming that concern equals resistance.

Concern may indicate rising decision pressure.

A buyer asking about risks may be closer to action than a user asking for definitions. An executive asking about failure modes may be more serious than someone asking for trends. An investor asking about monetization risk may be closer to a decision than one merely asking about market size.

In S2, the key question is:

Are concerns preventing action, or are they helping the market prepare for action?

When responsibility becomes central, the market moves toward S3.

S3 Accountability Search

“Who Should Decide, Pay, Act, Regulate, or Own This?”

S3 is one of the most important stages in the model.

At this point, the market begins assigning responsibility.

The questions change from “What is this?” and “What are the risks?” to:

Who should act?

Who should pay?

Who should decide?

Who should regulate?

Who should own this internally?

Which team is responsible?

Which provider should we trust?

Who is accountable if this fails?

This transition matters because accountability is close to action.

A market that is assigning responsibility is no longer merely observing. It is preparing for commitment. The decision is becoming real enough that someone must own it.

In B2B markets, S3 may show up through budget-owner searches, vendor comparisons, procurement questions, implementation guides, compliance requirements, or internal ownership discussions. In investment markets, it may appear as serious category evaluation, diligence frameworks, and capital allocation debates. In public or regulatory markets, it may appear as pressure on institutions, regulators, companies, or governments to act.

S3 is powerful because responsibility changes behavior.

When no one is responsible, topics remain abstract. When responsibility appears, action becomes more likely.

The danger in S3 is underestimating irreversibility. Once accountability becomes dominant, markets can move quickly. Competitors may reposition. Buyers may create budgets. Regulators may intervene. Investors may reprice categories. Customers may shift expectations.

From a decision-intelligence perspective, S3 often marks the point where waiting becomes costly.

The key question is:

Is accountability creating a path toward commitment, or is responsibility being avoided?

If accountability leads to action, the market enters S4.

S4 Action / Enforcement

Decisions Become Visible

S4 is the stage most organizations notice.

Budgets are allocated.

Contracts are signed.

Policies are created.

Products are adopted.

Markets are entered.

Regulations are enforced.

Competitors react.

Customers change behavior.

At this stage, the decision environment has become visible as market behavior.

Traditional research is often strongest here because outcomes can be measured. Revenue appears. Adoption increases. Competitor movement becomes obvious. Search behavior becomes more transactional. Case studies appear. Benchmarks become available. The market feels real because action is visible.

But from a strategic standpoint, S4 is late.

By the time action is obvious, the strongest early positioning opportunities may already be gone. Competitors may have established authority. Buyers may have formed preferences. Pricing expectations may have stabilized. Search results may be harder to penetrate. Investor attention may have increased valuations. Strategic flexibility may have declined.

This does not mean S4 is unattractive. Many strong businesses are built in markets that have already reached action. But the decision logic changes. The opportunity is no longer based on early detection. It is based on execution quality, differentiation, trust, and structural advantage.

In S4, the key question is:

Can the organization compete effectively now that the market is acting?

If action becomes routine, the market moves to S5.

S5 Normalization

The Decision Becomes Expected

In S5, the behavior no longer feels like a decision.

It becomes normal.

Customers expect the category to exist. Companies assume the function is necessary. Investors understand the market logic. Regulators may have defined boundaries. Buyers know how to compare options. The market has moved from uncertainty to expectation.

At this stage, the original question disappears.

People no longer ask whether the category is real. They ask which option to choose, how much to spend, which provider is credible, what level of performance is acceptable, and how to optimize the decision.

Normalization changes competitive dynamics. Differentiation becomes harder. Buyers become more informed. Category language stabilizes. Content becomes more competitive. Trust signals matter more. Pricing pressure may increase. Brand, authority, operational excellence, and proof become more important.

S5 markets can be very profitable, but they are rarely easy.

The opportunity is no longer to prove the category. The opportunity is to win within it.

In S5, the key question is:

What structural advantage allows a company to capture value in a market where the decision has already normalized?

Dangerous Transitions

Not all state transitions are equal.

Some transitions create unusual strategic risk because they indicate that the market is moving faster than institutions, companies, or investors expect.

One dangerous transition is S1 to S3. This happens when a market skips deep evaluation and moves quickly from legitimacy questioning to accountability. People stop asking whether the topic is real and begin asking who should act. This can create sudden pressure on companies, regulators, or category leaders.

Another dangerous transition is S2 to S4. This happens when harm, cost, or risk framing moves directly into action. Concern becomes intervention. In commercial markets, this may appear as rapid buyer shifts or abrupt rejection of a category. In regulatory markets, it may appear as enforcement. In investment markets, it may appear as repricing.

A third dangerous transition is S3 to S5. This happens when accountability becomes normalized before local systems have fully adapted. A behavior becomes expected elsewhere, and the local market begins treating adoption as inevitable. This can create institutional lag, where decision pressure rises faster than organizations are prepared to respond.

These transitions matter because they affect timing.

Early-stage markets are not always slow. Mature markets are not always stable. A market can move suddenly if the decision state changes quickly.

Market Decision Intelligence therefore monitors transitions, not only static conditions.

The question is not only where the market is.

The question is how quickly the market is moving between states.

Decision States and Business Strategy

Decision States help organizations avoid one of the most common strategic errors: applying the wrong strategy to the wrong stage.

A market in S1 needs education, legitimacy, and conceptual clarity. A market in S2 needs risk reduction, consequence framing, and trust. A market in S3 needs ownership, decision support, comparison, and accountability. A market in S4 needs execution, differentiation, and conversion pathways. A market in S5 needs authority, proof, and defensible positioning.

If the market is in S1 and the company behaves as though buyers are in S4, it will push for conversion before the market is ready. If the market is in S4 and the company remains stuck in educational content, it may attract attention but lose decision-stage demand. If the market is in S3 and the company does not clarify ownership, buyers may hesitate because responsibility remains unresolved.

This is why understanding decision state is not theoretical.

It changes how markets should be evaluated.

It changes what content matters.

It changes what risks matter.

It changes what competitors matter.

It changes whether investment is premature, timely, or late.

For YNALIZE, the decision-state lens is especially important because the firm’s work is not designed to optimize visibility in isolation. It is designed to reduce decision risk before growth, SEO, or market-entry investment. That requires knowing not only whether demand exists, but whether the market has reached a state where responsible action is possible.

A market that is visible but stuck in S1 may not justify major commitment.

A market moving from S2 to S3 may require urgent strategic evaluation.

A market already in S5 may require a different kind of competitive analysis.

The state changes the decision.

From Decision States to Decision Boundaries

Decision States explain where the market is in its readiness journey.

Decision Boundaries explain whether action is justified.

The two concepts work together.

A market may be in S2, showing serious concern and evaluation, but still fail the monetization boundary. A market may be in S3, showing accountability pressure, but fail the execution boundary. A market may be in S4, showing visible action, but fail the competitive boundary because attention is already controlled by dominant players.

This is why Decision States alone are not enough.

They reveal readiness.

They do not automatically justify commitment.

The next step is to test whether the market has crossed the boundaries required for responsible action.

That is the role of the Decision Boundary Framework. YNALIZE Methodology

Comments